Real Estate's Rise

U.S. home prices are up 18.8% over the past 12 months. That’s well above the highest year-over-year rate (14%) notched leading up to the bursting housing bubble in 2008.

U.S. home prices are up 18.8% over the past 12 months. That’s well above the highest year-over-year rate (14%) notched leading up to the bursting housing bubble in 2008.

But housing economists are clear: This frenzy will eventually end. Simple economics dictates that home price growth can’t outpace income growth forever. At its latest reading, home prices were growing six times faster than wages.

The housing market will eventually cool. That’s the good news. The bad news? All signs point to the housing boom continuing through at least the spring housing market we’ve just entered.

The past decade’s booming residential real estate market has enriched every U.S. homeowner, with the large gains benefiting the wealthiest of us, according to a new paper. From 2010 to 2020, about 71% of the gain in housing wealth went to high-income households, according to the National Association of Realtors.

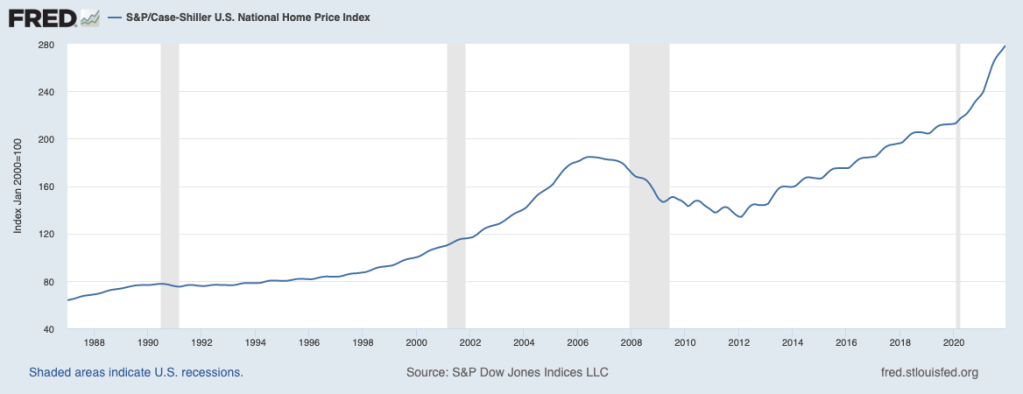

Overall, the total value of owner-occupied homes in the U.S. rose $8.2 trillion over the last ten-plus years to $24.1 trillion, NAR said. Those wealth gains have persisted in the past two years, as housing prices have surged due to robust demand and limited supply. This surge in home prices is not a new trend. Looking at the long-term home price data below it is clear that demand (demographics) and inflation are pushing on home prices.

S&P/Case-Shiller US National House Price Index in the United States

Home prices are rising quickly in a simple supply-demand imbalance. Or is it? Inventory of homes is at a multi-year low. (see below) High demand, low supply equal rising home prices. Fair enough. I remember this equation from macroeconomics class in college.

Rising interest rates cause the annual cost of housing to rise which should work against home buyers pushing down demand.

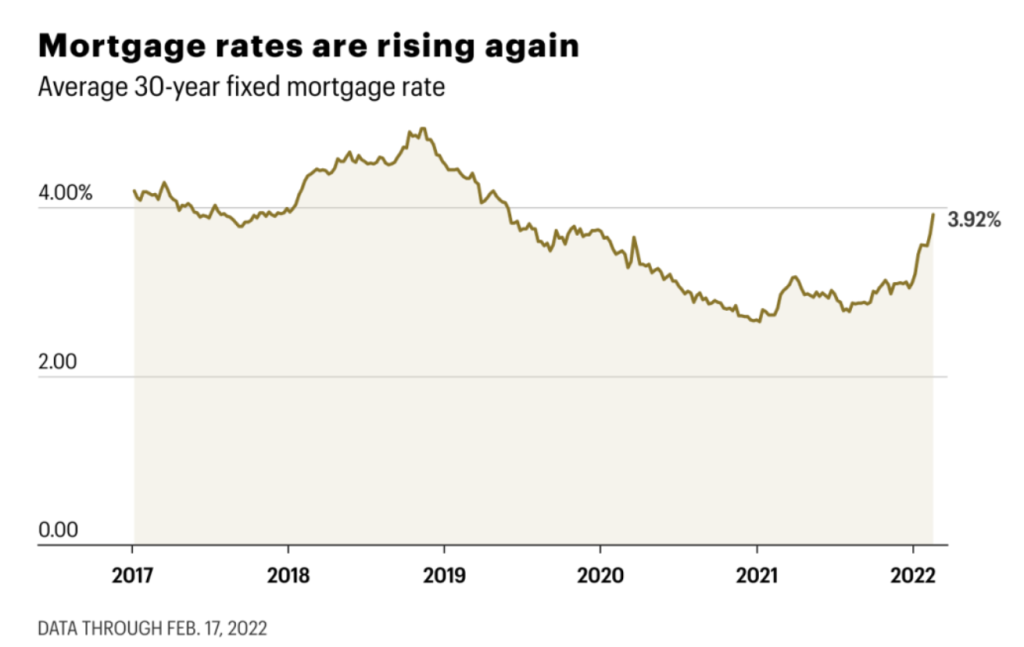

Freddie Mac forecasts a deceleration in the coming quarter for home prices. (see chart below) Given that 18.8% was a record, it seems like a safe bet to forecast lower price growth. Add in the rise in interest rates, home price rises should definitely decelerate. Right?

Anytime we assess a market’s forces or the direction of crowd movement it is important to look at special circumstances driving price change. A change in information often leads to a change in price. The inventory change of homes by neighborhood is a troubling “special circumstance”. Rural and Suburban inventory of homes plunged over the last 3 years dropping 40%. (see chart below) A trend that started before the COVID-19 pandemic has accelerated. Homebuilders will struggle to fill the gap. It takes years to buy land and start new construction. This supply-demand imbalance will forces home prices up, even in the face of rising interest rates. A serious tug of war will ensure. Unless buyer’s capacity to spend is diminished by falling wages.

Even though interest rates are rising for the first time in many years, mortgage rates are at historical lows when compared to the last 50 years. Supported by low mortgage rates, homeownership blossomed in the 1990s then started to vanish after 2005. (compare the two graphics below)

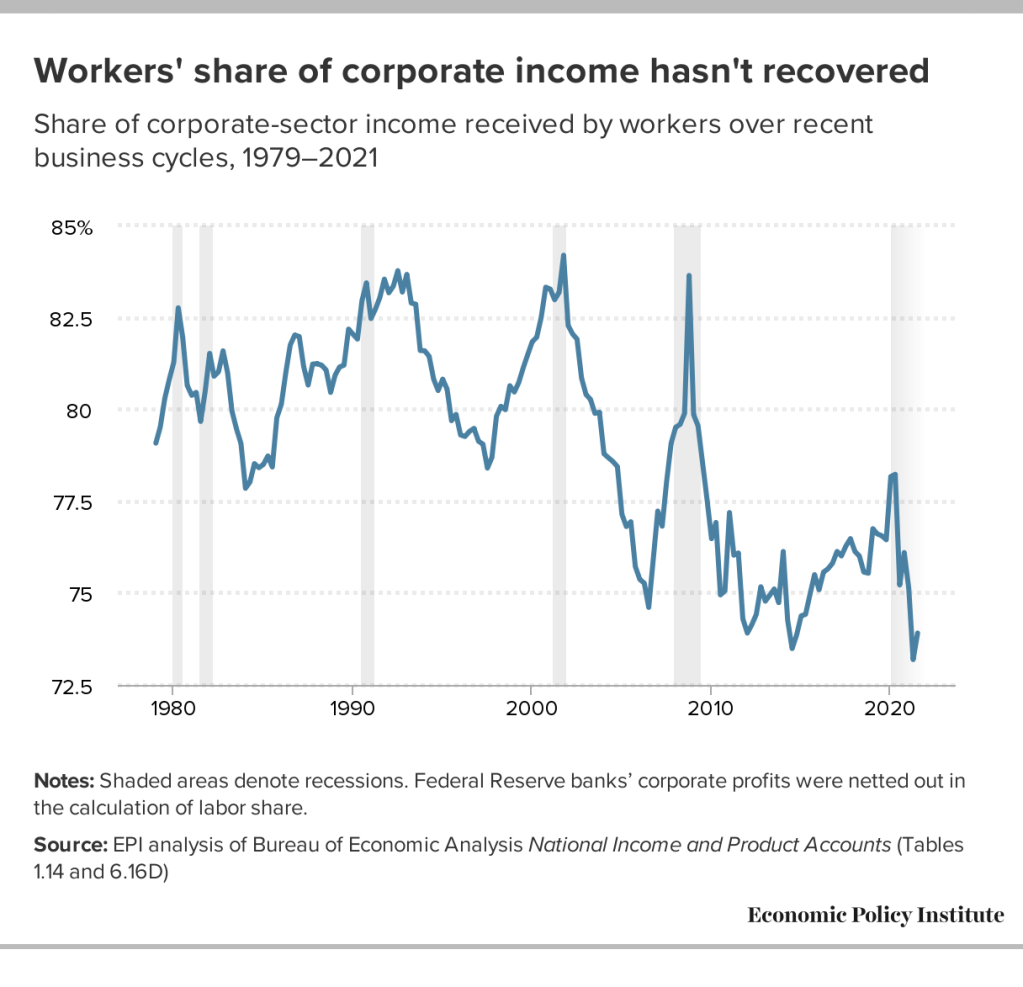

The challenge for homeownership and rising home prices will be the fall in wages. The graphic below paints an ugly picture of “workers’ share of corporate income” which is a better model of wages and potential wage growth. In the long run, wage growth and stability are the primary drivers of homeownership, as assuming debt is a bet on the future. However, in the short run homes are considered a safe investment with the hope of price appreciation. This last big push in home prices might have been pure speculation on the part of the average American. Fear of rising interest rates coupled with the COVID-19 pandemic likely drove the exodus to the suburbs.

Do the excesses in the residential real estate market signal a speculative bubble that will one day pop? Probably. Excesses tend to wind their way out of the system over time or overnight. Overnight price swings can be catastrophic. I would be a seller of residential real estate, not a buyer. You might want to re-think your purchase of a castle. At least for now.

If you have the opportunity to migrate from the inner city to the suburbs or downsize, now feels like the right time. I will be the first to admit, with an illiquid market like housing, getting a read on the crowd’s intention is tough.

Until next time. Stay frosty.